Adnoc CEO backs AI to stimulate energy sector growth

4 November 2024

Register for MEED's 14-day trial access

Sultan Ahmed Al-Jaber, managing director and group CEO of Abu Dhabi National Oil Company (Adnoc Group), has highlighted the interconnectedness of energy and artificial intelligence (AI) and its potential to transform energy systems.

In his keynote address at the Abu Dhabi International Petroleum Exhibition and Conference (Adipec), Al-Jaber appealed for an integrated, cross-sectoral response to meet the fast-growing energy needs of AI.

Al-Jaber, who is also the UAE's Industry & Advanced Technology Minister, said that the UAE has built an AI ecosystem that is fostering growth and low-carbon development.

He said the adoption of AI is also accelerating Adnoc’s growth strategy.

“For Adnoc, AI stands for applied intelligence. We chose to be one of the earliest adopters, because we saw it as a strategic imperative to drive efficiency, unlock value, enhance growth, lower emissions and future-proof our business,” he said.

Al-Jaber also announced the launch of ENERGYai (Energy to the Power of AI), a new AI system that Adnoc has developed in partnership with Abu Dhabi-based firms AIQ and G42, as well as technology giant Microsoft. The platform will be the first to apply agentic AI at scale within the energy industry and is capable of autonomously analysing vast datasets, making real-time decisions and driving operational improvements.

ALSO READ: Adnoc publishes report on role of AI in energy

ENERGYai will combine large language model technology with AI agents that are trained in specific tasks across Adnoc’s value chain.

These specialised AI agents bring autonomy and precision to critical tasks, from seismic analysis to energy efficiency and real-time process monitoring. Designed for seamless integration into existing workflows, the agents harness machine learning and predictive analytics, improving decision-making and operational efficiency.

Built using 80 years of Adnoc’s data, the three-year development programme for ENERGYai will begin testing with real-world datasets by the end of 2024 in several specific areas. It is projected that the system will cut by up to 75% the time it takes to build detailed geological models using very large and diverse datasets to support planning and development of large-scale carbon dioxide storage solutions.

In development planning, Adnoc says the new AI system will accelerate plans from one to two years to weeks, minimising costs and emissions in the process. It can analyse several scenarios in parallel, and this ability to run detailed, advanced simulations across all variables helps make faster and more accurate decisions.

Further along the value chain in the downstream business, the future-proof and scalable design of ENERGYai integrates with Adnoc’s existing technologies and platforms.

“It will not only analyse petabytes of data, it will proactively and autonomously identify operational improvements. It will perceive, think, learn and act. It will speed up seismic surveys from months to days. It will increase the accuracy of production forecasts by up to 90%. And it will be a powerhouse for value creation, efficiency and sustainable energy production that can benefit the whole industry,” Al-Jaber said.

Energy trends

AI is among three "megatrends" in the global energy sector that Al-Jaber highlighted in his opening remarks at Adipec, with the other two being the rise of emerging markets and energy system transformation. He said that harnessing the megatrends requires unprecedented cross-sectoral integration to accelerate sustainable growth.

Al-Jaber noted that targeted investment, enhanced grid and energy infrastructure and enabling policies and regulations are crucial to unlocking the transformative potential of the megatrends.

Adnoc, he added, is embracing the megatrends and pivoting to new opportunities across the energy value chain and around the world to future-proof its business, decarbonise and deliver long-term sustainable value.

He said that by 2050, the world’s population will grow by a further 1.7 billion, mostly in the Global South, and as a result, energy markets must shift and grow, and energy systems must be transformed.

“Wind and solar will expand seven times. Liquefied natural gas (LNG) will grow by 65%. Oil will continue to be used for fuel and as a building block for many essential products. And as the world becomes increasingly urban, demand for electricity will double.

“Adding to this demand is AI. AI is one of those era-defining breakthroughs that is changing the pace of change itself. It is redefining the boundaries of productivity and efficiency. And it has the potential to accelerate the transformation of energy systems and to supercharge low-carbon growth.

“But the exponential growth of AI is also creating a power surge that no one anticipated 18 months ago. That’s when ChatGPT took off. A single prompt on ChatGPT needs 10 times more energy than a Google search. As AI expands, it will rely on a massive scale-up of data centres for its huge and fast-growing computational needs. Over the next six years, data centres will more than double, requiring at least 150GW of installed capacity by 2030 and double that again by 2040,” Al-Jaber said.

He noted that no single source of energy is going to be enough to cater to this demand, and that meeting this demand sustainably will require harnessing diverse energy sources, from renewables and nuclear to LNG, alongside advanced infrastructure and increased investment.

“We need more infrastructure that is fit for purpose and fit for the future. We need investment in the power sector to grow to at least $1.5tn per year. We need enabling policies and regulations to accelerate and protect those investments. And we need to leverage AI’s potential to optimise energy sources, predict peaks and dips in demand and enhance battery storage,” Al-Jaber said.

“The train is leaving the station. What we decide right now will decide our destiny. This is a moment that will separate leaders from those who are left behind. And, when called on to lead, this industry always steps up,” he concluded.

Photo credit: Adnoc via

Register for MEED's guest program now to access this article.

Exclusive from Meed

-

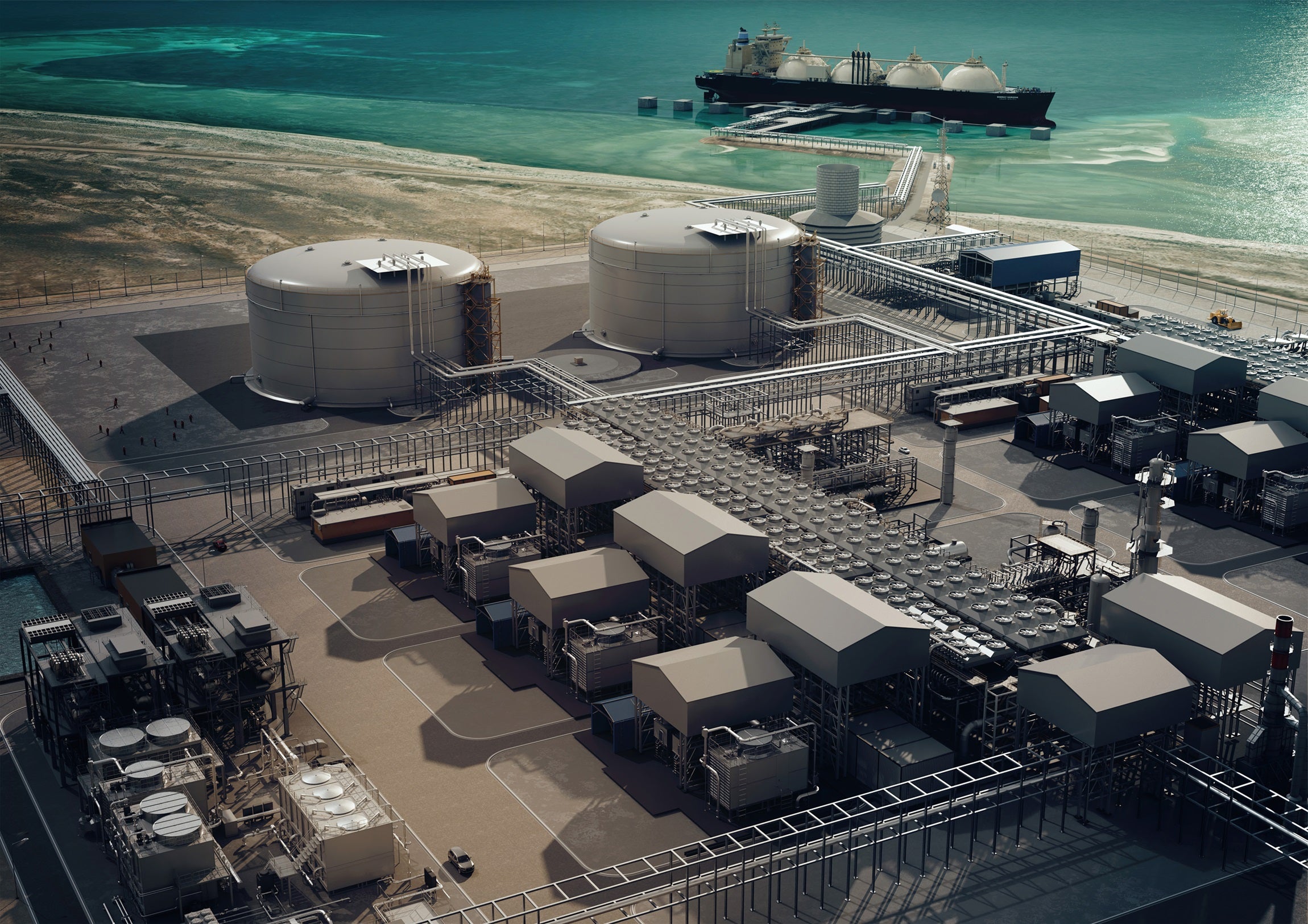

Qatar’s new $8bn investment spices up global LNG race

Qatar’s new $8bn investment spices up global LNG race13 March 2026

-

Bahrain opens bids for first solar IPP project

Bahrain opens bids for first solar IPP project13 March 2026

-

-

Frontrunner emerges for Saudi sewage treatment project

Frontrunner emerges for Saudi sewage treatment project13 March 2026

-

Medina tenders Sikkah Al-Hadid PPP project

Medina tenders Sikkah Al-Hadid PPP project13 March 2026

All of this is only 1% of what MEED.com has to offer

Subscribe now and unlock all the 153,671 articles on MEED.com

- All the latest news, data, and market intelligence across MENA at your fingerprints

- First-hand updates and inside information on projects, clients and competitors that matter to you

- 20 years' archive of information, data, and news for you to access at your convenience

- Strategize to succeed and minimise risks with timely analysis of current and future market trends

Related Articles

-

Qatar’s new $8bn investment spices up global LNG race

13 March 2026

In the midst of the conflict between Iran and the US and Israel, which has spilled over into the GCC region, QatarEnergy has temporarily halted production of liquefied natural gas (LNG) in the country and declared force majeure on LNG shipments after its energy assets came under attack.

When the fog of war clears, however, and the Strait of Hormuz reopens to oil and gas flows, the global economy will look to QatarEnergy to swiftly restore regular LNG cargoes in order to bring gas prices down from record highs.

Beyond that short-term role, the recent $8bn investment the Qatari giant has committed to building two new LNG processing trains will also cement its position as a reliable long-term supplier, while further intensifying the race among global LNG producers to carve out larger market shares in an increasingly gas-hungry world.

North Field West – a game changer

The state-owned company has progressed from the front-end engineering and design (feed) phase to the engineering, procurement and construction (EPC) stage of its North Field West LNG project at pace.

It awarded the main EPC contract for the scheme – covering two LNG processing trains with a total capacity of 16 million tonnes a year (t/y) – to a joint venture comprising France’s Technip Energies, Greece/Lebanon-based Consolidated Contractors Company (CCC) and Gulf Asia Contracting on 25 February.

The contract, estimated to be worth $8bn, was awarded just a month after Japan-based Chiyoda Corporation won the project’s feed contract.

Such a short interval between the feed and EPC phases for a project as large as North Field West LNG would typically be considered improbable. Industry sources suggest QatarEnergy may have been in discussions with Chiyoda and the Technip Energies-CCC consortium for at least a year regarding the feed and EPC contracts, respectively – particularly given the two-year gap between the project’s announcement in February 2024 and the start of the EPC phase.

Chiyoda, Technip Energies and CCC are also involved in the first two phases of QatarEnergy’s $40bn North Field LNG expansion project. A consortium of Chiyoda and Technip Energies is executing EPC works on the North Field East project, which involves the construction of four LNG trains with a combined capacity of 32 million t/y, following the award of a $13bn contract in February 2021. Meanwhile, a Technip Energies-CCC consortium is carrying out EPC works on two 7.8 million t/y LNG trains as part of the North Field South project, having secured a $10bn contract in May 2023.

More significant, however, is the speed with which QatarEnergy is advancing its strategic objective of reaching a total LNG production capacity of 142 million t/y by the end of the decade, from 77.5 million t/y at present.

With all three phases of the North Field LNG expansion programme now under EPC execution – and North Field East scheduled for commissioning later this year – QatarEnergy appears firmly on track to become one of the world’s largest LNG suppliers over the long term, reinforcing Qatar’s economic future in the process.

US domination

While QatarEnergy is on course to increase its LNG production capacity by 83% by 2030 through the overall North Field LNG expansion programme, it is still some way behind the US, which is set to account for over half of the total global LNG liquefaction projects by 2030.

There are 40 new-build and expansion LNG liquefaction projects planned or under way in the US, according to UK analytics firm GlobalData. Among these, two projects stand out.

The first is the Rio Grande LNG production project, being developed by NextDecade in Texas, on the US Gulf of Mexico coast. Up to 10 processing trains are planned for the complex, the first three of which are in the EPC phase.

NextDecade achieved the final investment decision on the fourth and fifth trains at the facility, estimated to cost $6.7bn each, in September and October last year. The company has awarded EPC contracts to build all five trains at the Rio Grande facility to US-based Bechtel.

On the investments front, the overseas-focused energy investment vehicle of Abu Dhabi National Oil Company (Adnoc), XRG, acquired an indirect 11.7% stake in the first phase of the project from Global Infrastructure Partners (GIP), part of US asset manager BlackRock, in September last year. In February 2026, XRG entered into another transaction with GIP to raise its overall participation in the Rio Grande LNG project by acquiring additional 7.6% equity interests in trains four and five of the scheme.

Additionally, as part of that transaction, another Adnoc Group subsidiary, Adnoc Trading, entered into a 20-year offtake agreement with NextDecade last year to purchase 1.9 million t/y of LNG from Rio Grande train four, on a free-on-board basis at a Henry Hub-indexed price. France’s TotalEnergies and Saudi Aramco are the other LNG offtakers for train four.

Separately, the Commonwealth LNG facility in the US state of Louisiana has also received backing from Abu Dhabi. Expected to start operations in 2030, the facility is designed to produce up to 9.5 million metric t/y of LNG.

Commonwealth LNG is a project of US-based alternative asset manager Kimmeridge Energy Management Company and Abu Dhabi’s sovereign wealth fund Mubadala Investment Company through their joint venture Caturus.

Caturus was formed in August 2025 when Kimmeridge announced a rebranding that saw Commonwealth LNG and Kimmeridge’s upstream operations combined under a new integrated platform. At the same time, Mubadala acquired a 24.1% equity stake in Caturus, providing financial backing for the new entity to proceed with the Commonwealth LNG project.

Also in August, Caturus awarded Technip Energies the contract for EPC works on the Commonwealth LNG project. The French contractor had previously performed the project’s feed work.

Moreover, Aramco subsidiary Aramco Trading signed a 20-year agreement to buy 1 million metric t/y of LNG from the Commonwealth LNG facility in February, increasing offtake deals secured by Caturus to cover 8 million metric t/y of the project’s total planned output capacity.

Positive outlook

The growth in LNG production capacity in the US, as well as in wider North America, is driven by several factors, including abundant natural gas reserves, the shale gas revolution and advancements in hydraulic fracturing and horizontal drilling.

While it might be a challenge for QatarEnergy to compete with US players in combined liquefaction capacity, its strength and success will lie in clinching long-term offtake deals with customers in Asia, where the bulk of global LNG demand growth is expected.

https://image.digitalinsightresearch.in/uploads/NewsArticle/15954252/main3511.jpg -

Bahrain opens bids for first solar IPP project

13 March 2026

Two companies have made offers for a contract to develop Bahrain’s first solar photovoltaic (PV) independent power project (IPP).

Bahrain’s Electricity & Water Authority (EWA) opened bids for the Bilaj Al-Jazayer solar IPP project on 12 March.

The bidders include Saudi Arabia’s Acwa, formerly Acwa Power, and UAE-headquartered Yellow Door Energy.

The 150 MWac Bilaj Al-Jazayer solar IPP project will be Bahrain’s first grid-connected solar PV power plant developed under a public-private partnership (PPP) framework on a build-own-operate basis. It will be delivered as a long-term concession and is intended to come online by 2027.

The proposed site covers more than 1 square kilometre, with the private sector responsible for end-to-end development, including financing, design, construction and operation.

Last August, EWA held a market consultation event during which it outlined plans for the country’s first solar PV IPP. The main contract was then tendered in October.

EWA said Yellow Door Energy’s proposal was “accepted with conditions”, but did not disclose further details.

The local KPMG Fakhro is the financial consultant, the US’ WSP Parsons Brinckerhoff is the technical consultant, and the UK’s Trowers & Hamlins is the legal consultant.

Bahrain’s clean energy targets, as set by its national plans, include 20% renewables by 2035, and net-zero emissions by 2060.

https://image.digitalinsightresearch.in/uploads/NewsArticle/15968088/main.jpg

https://image.digitalinsightresearch.in/uploads/NewsArticle/15968088/main.jpg -

DP World sees Red Sea port volumes rising as Hormuz shuts

13 March 2026

Register for MEED’s 14-day trial access

Dubai-based ports operator DP World is preparing for higher throughput at its Red Sea terminals as the Iran conflict approaches its second week, CEO Yuvraj Narayan said on Thursday.

With the Strait of Hormuz effectively closed and tanker attacks escalating, shipping movements into Gulf ports have fallen.

The disruption began after US and Israeli strikes on Iran, rattling energy and freight markets and cutting access through what is widely seen as the world’s most critical oil corridor.

Since most major Gulf ports rely on the narrow Strait of Hormuz, the shutdown is weighing on regional trade flows.

Narayan said Jebel Ali, DP World’s main hub in Dubai, has not suffered any infrastructure damage and is operating normally, but inbound vessel arrivals are down. Some cargo is still moving through terminals on the eastern side of the strait, he added.

Ports in the UAE that sit outside Hormuz have limited headroom to absorb the shortfall. Khorfakkan can handle about 5 million 20-foot equivalent units (TEUs) and Fujairah under 1 million TEUs, which Narayan indicated would not be enough to offset lost volume from Jebel Ali or Abu Dhabi’s Khalifa Port.

Jebel Ali alone processed 15.6 million TEUs last year, out of DP World’s 56.1 million TEUs globally.

DP World is rolling out rerouting options and other operational measures to keep supply chains moving. Narayan said the company’s Red Sea assets, such as Jeddah in Saudi Arabia and Sokhna in Egypt, are likely to see increased traffic, though he did not quantify the additional volumes or specify cargo types.

He cautioned that logistical and security risks remain elevated.

Earlier this week, DP World announced record financial results for 2025, with revenue up 22% to $24.4bn and adjusted earnings before interest, taxes, depreciation and amortisation (Ebitda) up 18% to $6.4bn, delivering a 26.3% margin, as MEED reported.

DP World said that this performance was driven by strong momentum across its ports and terminals and logistics business.

The group’s gross throughput rose 5.8% to 93.4 million TEUs.

Profit for the year increased 32.2% to $1.96bn, and operating cash flow grew 14% to $6.3bn.

Return on capital employed increased to 9.9% in 2025, up from 8.9% in 2024, reflecting stronger earnings despite ongoing geopolitical and trade uncertainty.

https://image.digitalinsightresearch.in/uploads/NewsArticle/15968045/main.jpg -

Frontrunner emerges for Saudi sewage treatment project

13 March 2026

A consortium led by China’s Jiangsu United Water Technology has emerged as the frontrunner for a contract to build and upgrade two sewage treatment plants in Saudi Arabia, according to sources.

The contract covers the North Western A Cluster Sewage Treatment Plants Package 11 (LTOM11), part of the next phase of National Water Company’s (NWC) long-term operations and maintenance (LTOM) sewage treatment programme.

The consortium comprising United Water, Prosus Energy (UAE) and Armada Holding (Saudi Arabia) offered “the lowest tariff” for the project, sources told MEED.

It is understood that Turkey’s Kuzu has made the next-lowest bid.

The development, estimated to cost about $211m, will have a combined capacity of about 440,000 cubic metres a day (cm/d).

In February, MEED exclusively reported that six bidders were competing for the contract.

The other companies that have submitted proposals include:

- Alkhorayef Water & Power Technologies (Saudi Arabia)

- Civil Works Company (Saudi Arabia)

- VA Tech Wabag (India)

- Aguas de Valencia (Spain)

LTOM11, also known as the North Western A Cluster, forms part of the second phase of NWC’s rehabilitation of sewage treatment plants programme.

The scheme is being procured on an engineering, procurement and construction (EPC) basis with a long-term operations component.

The main contract was tendered last year, with an award initially expected by the end of 2025.

It is now understood that NWC is preparing to offer the main contract in the second quarter.

As previously reported, Saudi Arabia’s NWC is also evaluating five bids for package 12 of its long-term operations and maintenance (LTOM12) sewage treatment programme.

Known as the North Western B Cluster, LTOM12 forms part of the second phase of NWC’s rehabilitation of sewage treatment plants programme.

In January, the same United Water-led consortium won the main contract for the Northern Cluster Sewage Treatment Plants Package 10 (LTOM10).

That project includes the rehabilitation and operation of nine sewage treatment plants located across the Hail, Qassim, Al-Jouf and Northern Borders provinces

NWC is also preparing to tender a contract for the construction of 10 sewage treatment plants as part of package 14 of the programme.

The final details of the Eastern A Cluster (LTOM14) package are being finalised, with a tender likely to be issued in March or April, sources told MEED.

READ THE MARCH 2026 MEED BUSINESS REVIEW – click here to view PDF

READ THE MARCH 2026 MEED BUSINESS REVIEW – click here to view PDFRiyadh urges private sector to take greater role; Chemical players look to spend rationally; Economic uptick lends confidence to Cairo’s reforms.

Distributed to senior decision-makers in the region and around the world, the March 2026 edition of MEED Business Review includes:

> RAMADAN: Data disproves the Ramadan slowdown story> INDUSTRY REPORT: Chemicals producers look to cut spending> INDUSTRY REPORT: Global petrochemical project capex set to rise until 2030> MARKET FOCUS: Egypt’s crisis mode gives way to cautious revival> LEADERSHIP: Delivering Saudi Arabia’s next phase of rail growth> INTERVIEW: Abu Dhabi’s Enersol charts acquisitions pathTo see previous issues of MEED Business Review, please click herehttps://image.digitalinsightresearch.in/uploads/NewsArticle/15968035/main.jpg -

Medina tenders Sikkah Al-Hadid PPP project

13 March 2026

Saudi entities including Al-Madinah Regional Municipality, in collaboration with the Ministry of Municipalities & Housing and the National Centre for Privatisation & PPP (NCP), have floated a request for proposal (RFP) notice for the development of the Sikkah Al-Hadid project.

The project will be procured through build-own-operate-transfer contracts with a 50-year duration, using a public-private partnership (PPP) model.

The deadline for bid submission is 23 June.

The project will be located to the west of Medina on an 84,657-square-metre (sq m) site.

It includes a four-storey medical centre with a capacity of up to 200 beds and a shopping mall offering retail, food and beverage, and other entertainment facilities.

In January last year, NCP asked firms to express their interest and prequalify for a contract to develop two mixed-use developments in Medina, which included the Sikkah Al-Hadid project and the Dhul Hulaifah project.

The Dhul Hulaifah project will be built on a 30,112 sq m site located six kilometres from the Prophet’s Mosque.

The development will consist of a four-star hotel integrated with retail and healthcare facilities.

MEED previously reported that Saudi Arabia had announced a P&PPP pipeline comprising 200 projects across 16 sectors.

This pipeline aims to attract local and international investors and ensure their readiness to participate in the schemes tendered to the market.

The initiative comes as the kingdom strives to increase the attractiveness of its economy and raise the private sector’s contribution to GDP.

https://image.digitalinsightresearch.in/uploads/NewsArticle/15968021/main.jpg