Damage avoidance frames debt issuance

22 April 2026

It is still early days, but Gulf fixed-income markets appear to have averted the worst of the conflict, with limited selloffs witnessed during the first six weeks of the Iran war.

This reflects a strong tailwind for GCC debt capital markets (DCM) in 2026, for both conventional and sukuk (Islamic bonds) – even if geopolitical turmoil may upend issuers’ best-laid plans.

Issuers started this year on the front foot, with Fitch Ratings recording $1.2bn in outstanding issuance as of 9 March, an increase of 14% in year-on-year terms, almost two-thirds of which is denominated in US dollars.

Those issuers were taking a long-lens view of their funding priorities looking forward. Despite that, there is a strong sense that Gulf markets have been hit harder than other emerging markets by the Iran conflict. For example, in the first trading week after the US-Israel attacks on Iran on 28 February, Asian investors were reducing their exposure to Gulf sovereign and corporate paper.

Pressure on sukuk

The impact on the sukuk market has been particularly pronounced. According to Fitch Ratings, the global sukuk market experienced a notable slowdown in dollar issuance during March, following strong activity in the first two months of 2026.

The impact on the sukuk market has been particularly pronounced. According to Fitch Ratings, the global sukuk market experienced a notable slowdown in dollar issuance during March, following strong activity in the first two months of 2026.

“If you look at the numbers for the first quarter of 2026 overall, the volume of sukuk issuance is slightly up, but the volume of issuance in FX [foreign exchange] is definitely down,” says Mohamed Damak, senior director, financial services at S&P Global Ratings.

“And the volume of issuance in FX in March was supported by some transactions that were announced before the start of the war.”

If there is a much more protracted conflict or with a much more severe implication on the economy, there could be a much more severe implication on the overall volume of issuance in the GCC. But the numbers as of the end-March indicate this is still not yet fully visible.

“The drop in the volume of issuance in FX is just 12% compared with March 2025, and the overall volume of issuance in local currency and foreign currency is still up by 2.3% year-on-year,” says Damak.

Strong foundations

Strong foundations

Last year proved an active one for Gulf DCM issuance. Overall, GCC countries accounted for 35% of all emerging market dollar debt issuance in 2025 (excluding China). According to Kuwait-based Markaz, primary debt issuances of bonds and sukuk in the GCC amounted to $189.47bn, through 515 issuances, up 28.13% on 2024.

“Prior to the conflict, GCC DCMs were performing strongly and building clear momentum,” says Bashar Al-Natoor, global head of Islamic finance at Fitch Ratings. “Most GCC issuers maintained robust market access throughout 2025 and into early 2026.”

Combined GCC issuance in January and February 2026 reached about $73bn, marking a 14.5% increase from the previous year, according to Fitch. “Sovereign and quasi-sovereign issuers remained foundational to the GCC DCM, but corporate and institutional participation was steadily rising, driven by favourable financing conditions,” says Al-Natoor.

Kingdom equation

Saudi Arabia made an auspicious start to 2026, raising $11.5bn on international markets in January, in a sale that was three times oversubscribed.

Saudi debt issuance forms part of the kingdom’s wider plans for increased borrowing, framed not just to plug a widening fiscal deficit, but also to take on a greater burden of debt repayment. The kingdom’s outstanding central government debt portfolio reached SR1.52tn ($405.15bn) by the end of 2025, about one-third of GDP.

The kingdom’s National Debt Management Centre’s long-term plan envisages 45%-60% of borrowing from domestic and international DCM, the latter comprising about $14bn-$20bn.

The Public Investment Fund sold $2bn of bonds on the London Stock Exchange in January, an issuance that was more than five times oversubscribed. In 2025, monthly Saudi debt issuance averaged $6.4bn a year, more than double the figure seen two years earlier.

Saudi banks’ interest in bonds is driven by a need to support loan activity, with credit outpacing deposits. Issuing bonds will help close a rise in the loan-deposit ratio, which is well above 100%.

“You would expect to see probably a lower level of issuance in Saudi Arabia, where the banks were contributing to a significant amount of issuance. They will probably see lower landing growth this year, which could result in lower overall refinancing needs,” says Damak.

The UAE is another prominent Gulf issuer that entered 2026 with a robust pipeline of DCM activity in the works.

Last year, issuance of $47.71bn absorbed a quarter of all GCC issuance, a 24% increase on 2024. That put it comfortably ahead of Kuwait on $23.7bn, and Qatar on $22.47bn, although one of the fastest increases in DCM issuance last year was from Bahrain, which raised $11.24bn, a 63% increase on the previous year.

UAE DCM was expected to exceed $350bn this year, notes Fitch Ratings, supported by strong sukuk issuance and the need to diversify funding sources. Dollar sukuk issuance in the UAE last year grew on 21.4% in 2024.

Ceasefire dependency

Much will inevitably hinge on the evolution of the Iran conflict. Here, it may pay to take the long-lens view, say analysts. “The liquidity declines observed in the Middle East and North Africa and GCC sukuk are unlikely to be permanent,” says Fitch’s Al-Natoor.

“As stability returns and the ceasefire holds, liquidity is expected to gradually recover, although the pace of recovery will be heavily dependent on investor confidence and sentiment.”

“As stability returns and the ceasefire holds, liquidity is expected to gradually recover, although the pace of recovery will be heavily dependent on investor confidence and sentiment.”

Al-Natoor emphasises that the market itself has not undergone a structural transformation. Instead, some investors have repriced risk and adjusted premiums to reflect heightened geopolitical uncertainty.

“This distinction matters, as the underlying fundamentals of GCC credit remain intact, with the majority of issuers holding stable outlooks. Notably, the number of GCC issuers placed on Rating Watch Negative increased during this period, reflecting elevated uncertainty.”

Rating Watch Negative flags that the rating is under review and could be resolved either by affirmation or downgrade, depending on subsequent developments.

“Perceptions and risk appetite may take time to recalibrate,” says Al-Natoor.

“Despite that, there has been some private placement activity during this period, which hints that investors may be selectively engaging with the market while monitoring developments.

“If current stability is sustained, a broader return to public markets could follow.”

This reinforces the sense that it is the sustainability and longevity of the ceasefire that will be decisive in shaping both the pace and strength of market recovery.

Fitch Rating’s base case leans towards gradual recovery in GCC DCM markets, both sukuk and conventional, rather than sustained structural damage.

“The fundamentals remain solid, but longer-term effects will ultimately depend on post-war sentiment and market access,” says Al-Natoor.

“We continue to see subdued dollar-denominated issuance, although some local currency activity persists.”

Register for MEED's guest program now to access this article.

Exclusive from Meed

-

AHS Properties acquires Shangri-La hotel for $300m

AHS Properties acquires Shangri-La hotel for $300m17 June 2026

-

Libya signs three oil deals after licensing round

Libya signs three oil deals after licensing round17 June 2026

-

Local consortium wins Egypt grid contracts

Local consortium wins Egypt grid contracts17 June 2026

-

-

All of this is only 1% of what MEED.com has to offer

Subscribe now and unlock all the 153,671 articles on MEED.com

- All the latest news, data, and market intelligence across MENA at your fingerprints

- First-hand updates and inside information on projects, clients and competitors that matter to you

- 20 years' archive of information, data, and news for you to access at your convenience

- Strategize to succeed and minimise risks with timely analysis of current and future market trends

Related Articles

-

AHS Properties acquires Shangri-La hotel for $300m

17 June 2026

Dubai-based real estate developer AHS Properties has announced the acquisition of the Shangri-La hotel for AED1.1bn ($300m), marking one of the largest single-asset real estate transactions in recent years.

AHS Properties acquired the hotel from local firm Mismak Asset Management.

The Shangri-La Hotel is a 43-storey, 200-metre tower located on Sheikh Zayed Road. Completed in 2003, it was among the first five-star hotels to open along the corridor.

The acquisition expands AHS Properties’ portfolio, which includes AHS Tower, a Grade A commercial development on Sheikh Zayed Road, and AHS City, the company’s master-planned mixed-use community on the same corridor.

In a statement, AHS Properties said that AHS Tower, AHS City and the Shangri-La hotel form a strategic “vertical corridor” platform, representing a significant portion of the company’s AED50bn development pipeline through the end of 2026.

“The transaction reflects AHS Properties’ strategy of deploying capital into high-quality, supply-constrained assets,” the statement added.

According to the Dubai Land Department, Dubai’s real estate sector recorded AED252bn in transactions in Q1 2026.

https://image.digitalinsightresearch.in/uploads/NewsArticle/17310101/main.jpg -

Libya signs three oil deals after licensing round

17 June 2026

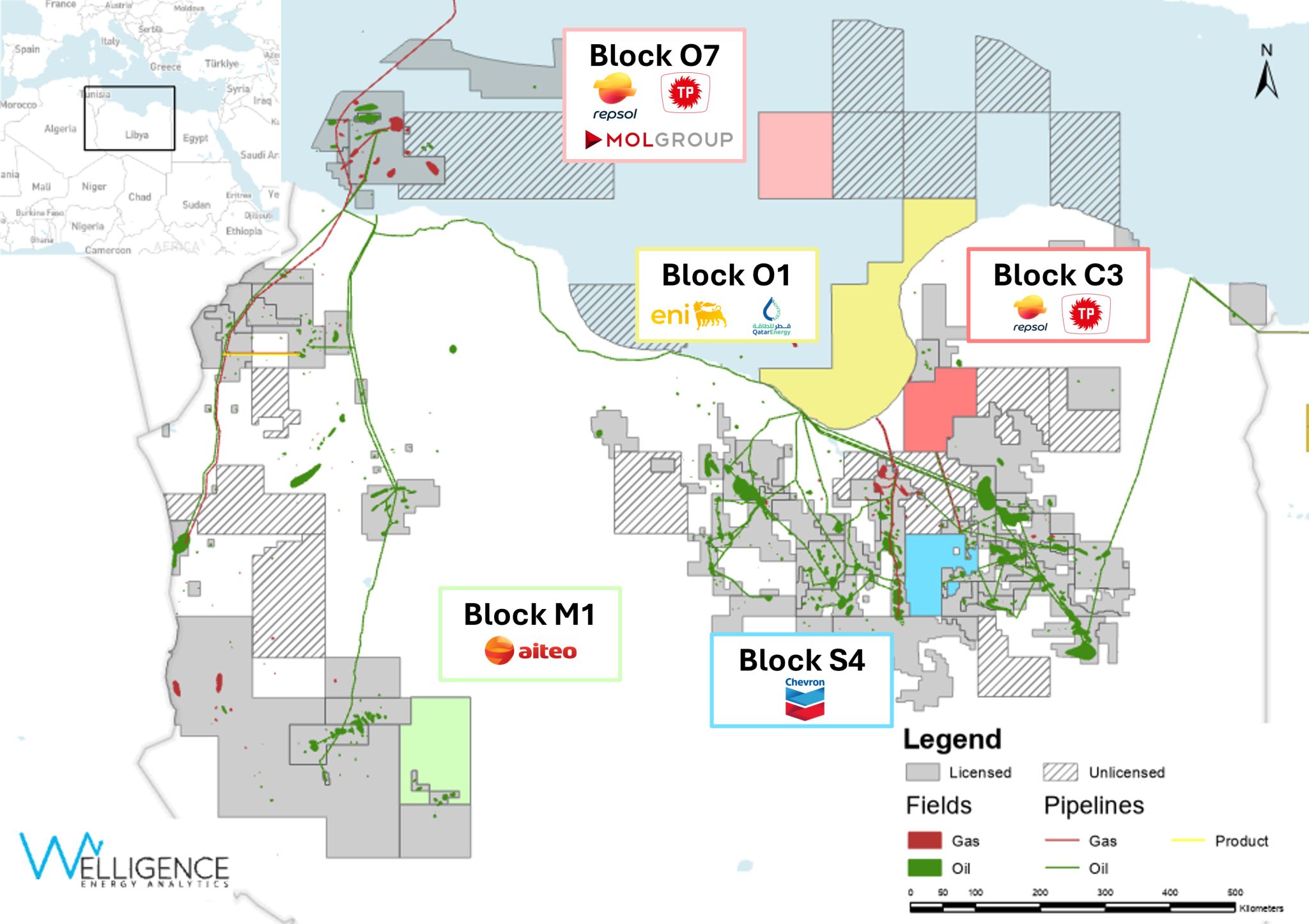

Libya’s National Oil Corporation (NOC) has signed three production-sharing agreements with several international energy companies following the country’s first licensing round in nearly two decades.

The three agreements have been signed with the following consortiums:

- Block O1 – offshore – Eni (Italy; 60%) and QatarEnergy (40%)

- Block O7 – offshore – Repsol (Spain; 40%), Turkiye Petrolleri A O (TPAO; Turkiye; 40%) and MOL Group (Hungary; 20%)

- Block C3 – onshore – Repsol and TPAO

The contracts are three of the five announced as awarded in February this year as part of the 2025 licensing round.

The three contracts were signed on 15 June.

It is not known why the remaining two awarded contracts have not been signed.

The remaining two contracts are:

- Block M1 – onshore – Aiteo (Nigeria)

- Block S4 – onshore – Chevron (US)

Libya is seeking to attract investment and raise oil production capacity to 2 million barrels a day (b/d) from around 1.4 million b/d currently.

The chairman of NOC, Massoud Suleman, said that the agreements reflected growing confidence in Libya’s oil and gas sector and would support exploration, development and production growth.

The 2025 licensing round was Libya’s first licensing round since 2007.

https://image.digitalinsightresearch.in/uploads/NewsArticle/17297353/main.jpg -

Local consortium wins Egypt grid contracts

17 June 2026

Egypt’s Korra Energi and High Dam for Electrical & Industrial Projects (Hidelco) have won contracts to build two sections of a major power transmission project connecting wind farms in the Gulf of Suez to the national grid.

The contracts were awarded by the Egyptian Electricity Transmission Company (EETC). In a statement, Korra said the contracts cover the first and third lots of a wider scheme involving the construction of 500-kilovolt (kV) extra-high-voltage overhead transmission lines.

The consortium will execute a 45-kilometre transmission line under Lot 1, valued at £E1.5bn ($29m).

Lot 3 covers a 52km transmission line and is valued at £E1.65bn.

The two contracts have a combined value of more than £E3bn ($58m). Both are scheduled for completion within one year of contractual close, Korra said.

The transmission lines will connect new wind power projects in the Gulf of Suez to Egypt’s electricity network. The project is expected to enable the integration of more than 2GW of renewable energy capacity.

The wider transmission scheme has an estimated investment value of £E12bn-14bn and has been divided into eight packages. EETC is implementing the project as part of efforts to strengthen grid infrastructure and increase its capacity to absorb renewable energy generation.

The award follows Korra Energi’s listing on the Egyptian Stock Exchange earlier this month. The company offered an 11% stake through a public and private placement at £E2.97 ($0.06) a share.

https://image.digitalinsightresearch.in/uploads/NewsArticle/17292020/main.jpg -

Retirement creates multibillion-dollar opportunity for region

16 June 2026

The GCC has long relied on government pension schemes and employer gratuity payments to provide for retirement. As workforces expand, demographics shift and expatriate communities put down longer-term roots, those arrangements are coming under growing strain. A new report from BlackRock argues that addressing those pressures represents one of the region’s more consequential economic policy opportunities – not only for individuals, but also for the depth and sophistication of its financial markets.

The asset manager’s recently published Read on Retirement: GCC 2026 study, based on a survey of 1,000 working individuals across the UAE and Saudi Arabia, depicts a workforce that is motivated but structurally underserved.

In the UAE, the survey finds that 78% of workers feel positive about their current financial position. Yet 59% say financial worries prevent them from planning for the future, and 58% worry about outliving their savings. Retirement preparedness stands at 67% among UAE nationals, underpinned by public pension provision, but falls to 46% among expatriates.

Three-quarters of respondents say they have begun preparing for retirement. Yet only 24% are contributing to a pension or long-term savings plan. The remainder are saving through cash, gold and property – assets that may preserve value but are not designed to generate sustainable retirement income. The survey indicates that 49% of respondents hold savings in cash, 40% in gold and 18% in property, suggesting a substantial share of potential long-term capital is held in short-term or non-productive forms.

“What we see in the data is a clear retirement knowledge gap, not an intention gap. People are doing the right things in principle, but they don’t yet have access to the types of investment frameworks that can deliver sustainable retirement outcomes,” says Kashif Riaz, head of Middle East financial markets advisory at BlackRock.

Good timing

Several factors have converged to make retirement reform a timely priority. The UAE’s population is young compared with other developed markets, which provides a wide window for building long-duration savings pools.

“It is a sweet spot right now – a very young population – and like all other geographies in the world, populations age over time,” Riaz says. “It is best to solve the problem structurally when the population is young and you have more workers than retirees.”

The character of the expatriate workforce is also changing. A growing proportion of overseas workers is making long-term residency decisions, shifting their financial planning accordingly.

“The demand for retirement solutions has grown much broader as expatriates make this their home for the long term,” Riaz notes. “Rather than conducting their banking, investing and primary real estate activity in their home countries with the intent to return, that is all happening here.”

Reform is already under way. The UAE has introduced an alternative end-of-service benefit framework allowing employers to shift from the traditional, unfunded gratuity model – where liabilities sit on employer balance sheets and assets remain uninvested – to funded, defined-contribution structures managed by licensed providers. The Dubai International Financial Centre’s (DIFC’s) Employee Workplace Savings scheme is the most developed operational example. The private sector is beginning to follow.

“Historically, in this region, only the largest or most multinational employers offered employee savings funds, but that is spreading,” Riaz says. “More insurance companies and asset managers are looking to develop the infrastructure to offer retirement solutions. We expect that to accelerate.”

Financial markets

For stakeholders in the region’s financial centres and for institutional investors, the big opportunity is what a well-established retirement system would mean for regional markets. The DIFC, Abu Dhabi Global Market and Saudi Arabia’s King Abdullah Financial District have each invested substantially in regulatory and institutional capacity to attract and manage long-term capital. A domestically generated pool of retirement savings would provide durable demand for the instruments and markets they host, spanning listed equities, sukuk, private credit and infrastructure funds.

“The bigger and more vibrant a retirement system in a country, the bigger and more vibrant that country’s financial markets will also be,” Riaz says.

There is a precedent. Australia’s superannuation system, built over three decades, is widely credited with transforming the depth and sophistication of Australian capital markets.

For regional fixed income, a domestic retirement pool would create a durable base of long-duration buyers for government and corporate sukuk issuances that currently depend heavily on international appetite. For listed equities, it would deepen liquidity on bourses in Dubai, Abu Dhabi and Riyadh. And for infrastructure, it would provide precisely the patient capital the growing regional PPP pipeline requires.

Favourable conditions

The retirement survey findings suggest unusually favourable demand conditions for reform. More than 90% of both UAE nationals and expatriates find defined-contribution workplace savings schemes appealing, with similar proportions indicating they would participate if such schemes were available. The main barriers are structural and informational rather than attitudinal. Only 13% of expatriates and 21% of nationals report confidence in understanding the retirement savings options available to them, while 92% say they would save more if given better incentives.

With 56% of respondents planning to increase their retirement savings, the case for directing that capital into more productive long-term channels is clear.

“By expanding access to funded, professionally managed workplace savings schemes, the UAE can not only strengthen financial outcomes for individuals, but also mobilise significant pools of domestic capital, allowing people’s savings to grow alongside the economy they are helping to build,” Riaz says.

https://image.digitalinsightresearch.in/uploads/NewsArticle/17289382/main.gif -

Gulf liquidity outpaces Syria’s financial reconnection

16 June 2026

Syria has the capital it needs to begin rebuilding. What it lacks is a banking system capable of moving that money at scale, and through 2026, the gap between the availability and mobility of funds has set the ceiling on recovery.

The capital itself is overwhelmingly Gulf and Turkish, deployed along clear lines rather than in a scramble. The $216bn rebuild estimated by the World Bank in its October 2025 damage assessment has room for several principals, and so far they are not competing for the same ground.

Qatar’s UCC Holding anchors two of the largest commitments: a $7bn power generation programme and a $4bn rebuild of Damascus International airport, both under contract since late 2025. The consortiums lean heavily on Turkish contractors, Cengiz and Kalyon among them.

Saudi Arabia’s package, announced in Damascus on 7 February, tilts to infrastructure and services: a SR7.5bn ($2bn) phased rebuild of Aleppo’s airports through the newly launched Elaf Investment Fund, and an STC fibre-optic and datacentre build worth more than SR3bn ($800m).

Regional diplomacy is taking precedence over the commercial carve-up: Turkish President Recep Erdogan and Saudi Crown Prince Mohammed Bin Salman agreed in Riyadh in early February to coordinate on Syrian reconstruction.

Abu Dhabi’s political embrace came more slowly than Riyadh’s or Doha’s – out of caution over the Islamist-led government– but the UAE’s major ports groups moved decisively.

Dubai’s DP World signed for Tartous in July 2025 and its 30-year concession went operational in mid-November. AD Ports followed on 6 November with a $22m purchase of 20% of the Latakia container terminal – run by France’s CMA CGM – which handles over 95% of Syria’s container volumes.

The wider UAE play has since broadened amid the US-Iran conflict in the Gulf, during which Syrian President Ahmed Al-Sharaa repeatedly voiced solidarity with the UAE.

In May, Dubai stepped up institutionally. Investment Corporation of Dubai managing director Mohammed Ibrahim Al-Shaibani met Al-Sharaa to discuss channelling UAE capital into real estate, tourism and financial services, while Abu Dhabi’s Eagle Hills presented plans for two urban schemes in Damascus and Latakia, with a reported budget of $50bn.

Syria’s railway establishment has meanwhile signed a framework with the Latakia terminal’s operators to study moving containers by rail to dry ports at Adra, Hisyah and Aleppo – the first thread connecting a Gulf-invested port to the inland network.

Certification is key

Saudi Arabia and Qatar cleared Syria’s $15.5m World Bank arrears in mid-2025, restoring its eligibility for grants. International financial institutions are reciprocating and returning, but cautiously – and not with a view to driving cash volume.

The World Bank portfolio comprises 10 grant-funded projects worth just over $1bn over three years. The approvals so far are foundational: a $146m electricity grant restoring transmission lines and 400kV interconnections with Turkiye and Jordan; $225m across two grants for water and health; and $20m for public financial management.

Transport is next in the queue rather than in hand. Syrian Transport Minister Yarub Badr said in June that Syria is seeking World Bank grants of between $65m and $200m for railway rehabilitation, to restore a transit corridor that reportedly moved up to 115,000 trucks a year between the Turkish and Jordanian borders before 2011.

Broader financing has not followed, however. The IMF’s February mission extended no loan programme, nor was lending discussed, despite the fund noting tight fiscal management and a 2025 budget surplus.

The IMF, and the World Bank alongside it, named the blockage: a banking sector that needs rehabilitating, central bank independence yet to be built, and restricted banking access still obstructing wider recovery.

Gulf backers, for their part, can commit capital in a signing ceremony, but they cannot readily push it through a system only beginning to reconnect to the outside world.

Piecemeal reopening

A few key developments have occurred. In November 2025, the central bank (pictured) sent its first Swift message in 14 years to the US Federal Reserve, and its dormant account there was reactivated. Visa and Mastercard processing then resumed in May after a 15-year hiatus.

These networks were never the key constraint, however. Correspondent banks must agree to clear Syrian transactions – and many institutions will likely continue to hold back on compliance and financial-crime grounds until proposed reforms are in place.

The moves by foreign banks have been expectedly thin as a result, and Doha has led. Qatar National Bank’s Syrian unit – a legacy presence that rode out the war – became the first to switch card acceptance on, while Qatar’s Estithmar Holding has taken a 49% stake in Syria’s Shahba Bank, becoming the sole new foreign equity entry into the sector so far.

The pound, trading near £Syr13,700 to the dollar, still sits slightly weaker than it did in 2024 – the last year of the old regime.

The fragility of the machinery showed again in May, when Al-Sharaa moved central bank governor Abdulkader Husrieh – who had overseen the Swift reconnection – to the ambassadorship to Canada; instead installing Safwat Raslan, the head of the state reconstruction fund, as his successor.

Some analysts read it as a sign of tension within the leadership over monetary policy and governance. It also flashed a warning: an institution the IMF wants independent had just changed hands at the president’s discretion.

At a June conference, the new governor pledged “institutional work and well-studied planning” with no “improvised or unilateral decisions”, defining himself against the tenure he replaced.

Raslan’s first measures constituted delays and institutional loosening. He reversed a Husrieh restriction that had confined the banknote changeover to bank branches – readmitting exchange companies and money-transfer firms – and extended the exchange deadline to the end of July. It marked the third such extension of a window first set at 90 days from the 1 January launch, with the original deadline having slipped by four months.

Conditional funding

The cashflow blockage is moulding Damascus’s financing strategy: take the institutions’ endorsement, but decline their direct lending, and lean on funding with fewer strings.

Rather than qualifying for an IMF programme and accepting its conditions, it is routing donor money through the Syrian Development Fund, which is now run by the man just made central bank governor – concentrating the reconstruction purse and monetary authority in one pair of hands.

The approach spares Syria a debt overhang, but it also leaves reconstruction dependent on Gulf commitments that arrive at the pace of politics rather than as drawable finance.

The near-term tests are already dated. The banknote changeover – at 63% as of early June – must close by 31 July, and the banking reforms specified by the IMF must be implemented.

If both hold, the pledged billions will gain a financial system to land in. If either slips, Syria’s reconstruction remains a stack of signed announcements waiting on the financial machinery to catch up.

This month’s special report on Syria also includes:

> PROJECTS: Momentum builds for Syrian projects

> OIL & GAS: Activity ramps up in Syria’s oil and gas sector

> CONSTRUCTION: Prospects improve for Levant constructionhttps://image.digitalinsightresearch.in/uploads/NewsArticle/17210681/main.gif